How Robinhood made a $57m mistake

The wonderful world of corporate actions

This week Robinhood ($HOOD) announced its Q4 results and included a stunning detail, they lost $57m due to an operational error when processing a corporate action.

What the heck!

Corporate actions can be anything from stock splits, dividends, mergers and acquisitions, spin-offs, and rights issues. They happen all the time but they usually don’t cause a $57m loss.

Cosmos Health ($COSM) was one of the 5,000 securities available on Robinhood’s platform and announced both a name change (from Cosmos Holdings to Cosmos Health) and a 1-for-25 reverse stock split. They announced the changes only a few hours before they came into effect. Surprise!

A reverse stock split is a reduction in the number of outstanding shares a company has. It’s typically based on a predetermined ratio. The share price changes proportionally and the market cap of the company remains the same. So why do this? Cosmos was trading below Nasdaq’s $1 share requirement and needed a reverse stock split to boost its share price and avoid a delisting.

Usually, stock splits are performed before the market opens. That way everything is accurately reflected in a customer's portfolio and they can happily go about their day. In some cases, if the split hasn’t been processed before the market opens then the stock is put into a view-only state, meaning you can see it but not place orders until it’s been sorted.

Unfortunately for Robinhood, it didn’t happen like that.

It appears that when the market opened Robinhood hadn’t processed the reverse stock split or changed the instrument state, meaning customers still had the old amount - which after the reverse stock split meant that customers saw 25x more Cosmos shares than they actually owned in their portfolio.

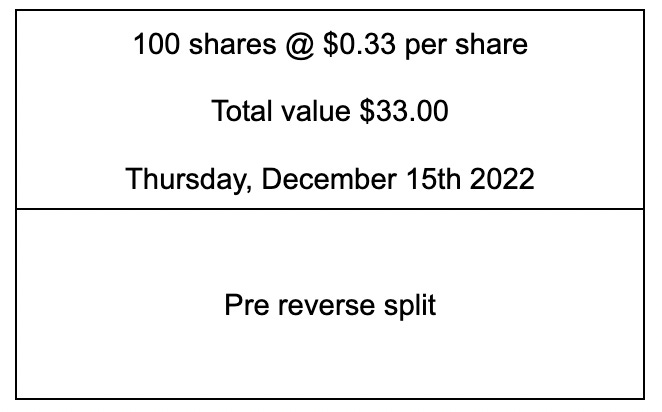

So, if you were a hypothetical Robinhood customer holding 100 Cosmos shares, your portfolio would have looked something like this:

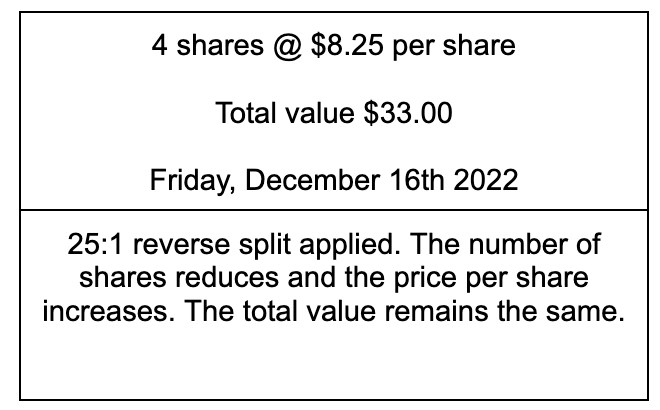

If Robinhood had realised the reverse split was occurring, this hypothetical customer portfolio should have been updated to:

Instead, this hypothetical Robinhood customer logged into their portfolio and saw this:

A few eagle-eyed customers must have noticed and successfully sold their huge windfall before Robinhood realised what was happening.

This is where it gets problematic for Robinhood. Robinhood sells 100 shares into the market, but only owns 4 because of the reverse split. The market doesn’t care or check to see if Robinhood actually has the shares because Robinhood has the responsibility to settle them.

You can sense where this is heading, a colossal headache. Robinhood is left holding the bag with a short position in Cosmos where they owe customers more than they actually hold. They have to buy back the shares they are short.

Things got even worse. Cosmos shares rallied on the day of the split from $8 to $24. Possibly attributed to huge short positions and meme stock interest. As a result, Robinhood bought back the shares they oversold (the difference between 100 they sold and 4 they actually had) at a cost of $57m.

Two months later Cosmos is now trading back down at $5 with a $53m market cap, so the Robinhood buyback is worth more than the entire company. Ouch!

Why didn't Robinhood wait to buy back the stock? Well, you can’t be short on customer assets as a broker. Also, imagine if the share price tripled again.

You can start to understand why corporate action processing is so complex. The information is fragmented and data quality is poor with lots of human oversight required. There’s also no standardisation to speak of.

So how the hell did this $57m mistake happen? Cosmos provided the perfect storm.

There was minimal notice of the corporate action. It’s likely Robinhood and its data providers had no idea about it. Usually, you’d get a notification from a third-party data provider who searches for these things. Most brokerages have multiple providers for redundancy. Why? Data providers often have incomplete information because they battle the same fragmentation as everyone else. These data providers use humans to trawl company announcements to compile information in one place.

The name change added to the confusion. It may seem like a minor detail but a name change requires a new CUSIP which is like a barcode or unique identifier for a US stock. This can throw backend systems and checks out.

Finally, there was lots of short seller and retail trader interest in the stock from customers who were paying much more attention than Robinhood was.

You have to wonder whether there is an opportunity for someone to make corporate actions data clean, clear, and accurate. Until that happens expect this kind of error to continue.

Edit: How would I solve this? I’d trigger an alert when a share price moves >100% in a day that requires a manual operator review and places the security in a view only state until the manual review is completed.

If you’re finding this content valuable, consider sharing it with friends, or subscribing if you haven’t already.

Corporate Actions alongside symbology management do introduce a lot of operational complexity into the system. People have been writing 3rd party tools/services to simplify this for years but it remains something that needs detailed attention. Good core system design is paramount, and it can be STP, but it needs to be designed to catch and flag errors/weird things intelligently, and there ultimately has to be a responsible operator investigating these issues, before the market opens - I don't think we could ever get away from that model.

Another major, somewhat related problem, is that of symbology changes. It's obviously a major risk if one is trading symbol:X and one is thinking one is trading symbol:Y, introduces the same price-risk of doing bad trades.